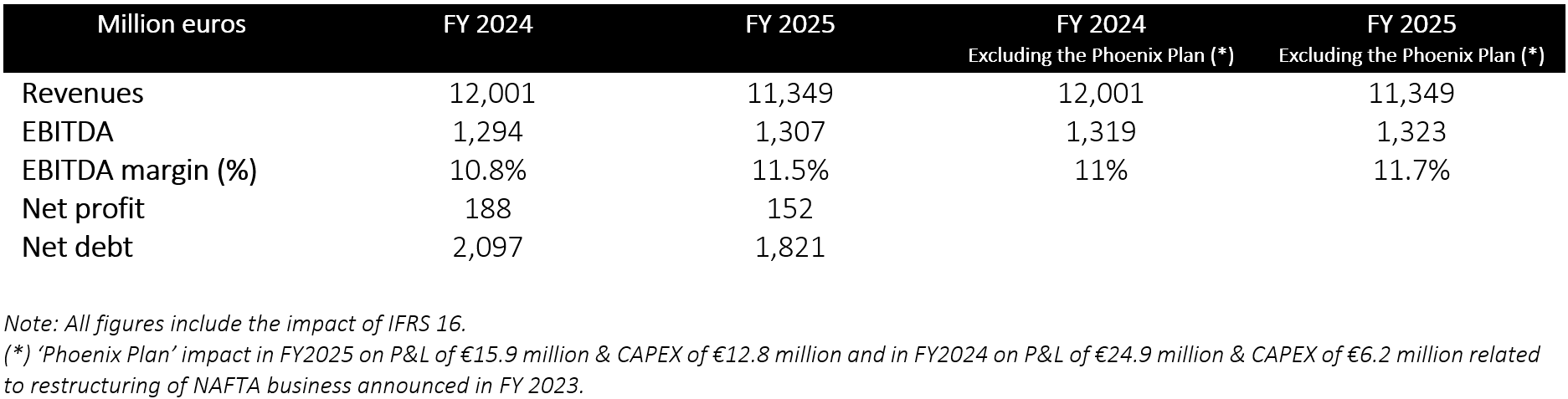

Gestamp, the multinational specialized in the design, development and manufacture of highly engineered metal components for the automotive industry, reported revenues of €11.3 billion in 2025, down 5.4% compared with 2024, due to a complex and uncertain industry environment marked by volatility in light vehicle production volumes, with declines in key regions such as Western Europe and NAFTA. The company’s revenue was also impacted by adverse foreign exchange rates in key markets where Gestamp operates.

Against this backdrop in 2025, a year marked by the realignment of electrification targets by several OEMs, Gestamp implemented extraordinary measures to adapt its strategy to a slowdown in electric vehicle adoption. In this context, the company entered into compensation agreements with certain customers, with a negative impact of €52 million at the EBIT level. These flexibility measures demonstrate the alignment between the company’s objectives and those of the manufacturers it works with.

Meanwhile, the company’s EBITDA amounted to €1.3 billion in 2025 (excluding the impact of the ‘Phoenix Plan’), in line with the 2024 figure. The rigorous operational efficiency initiatives, strict cost-control measures and profitability improvements implemented by the company enabled it to achieve an EBITDA margin of 11.7% at year-end 2025, representing an increase compared with 11% in 2024 (excluding the impact of the ‘Phoenix Plan’).

In this context, the company continued to make progress under its ‘Phoenix Plan’, which aims to bring NAFTA margins closer to those of the other regions in which it operates and to reach double-digit by 2026. In 2025, Gestamp met its targets and achieved a margin of 8.1%, up from 7% at the end of 2024.

The challenging industry environment also impacted Gestamp’s net income, which declined by 19% year-on-year to €152 million.

Francisco J. Riberas, Executive Chairman of Gestamp: “

The environment in which we operated in 2025 was once again marked by weaker vehicle production momentum in key global markets, driven, among other factors, by the slower penetration of electric vehicles, which, together with regulatory uncertainty, has impacted the company’s activity. Nevertheless, we have continued to protect Gestamp’s competitiveness through efficiency and cost-control measures, while also strengthening our balance sheet. This has enabled us to adapt to demand fluctuations, improve the profitability of our business and ensure sustained value creation for our stakeholders.”

Net debt declines to pre-IPO levels

During the year, the company continued to make progress in its debt optimization strategy to strengthen its financial position. In this regard, Gestamp reduced its net debt by €276 million over the year, to €1.8 billion as of the end of 2025. This represents the lowest indebtedness since the company’s IPO in 2017 and brings leverage to a net debt-to-EBITDA ratio of 1.4x, in line with the company’s target of maintaining it within a range of between 1.0x and 1.5x EBITDA.

Among the initiatives implemented in 2025 to strengthen the balance sheet and reduce debt, the closing in September of an agreement with Banco Santander stands out, under which the financial institution, through Andromeda Principal Investments, S.L.U., acquired a minority stake in the share capital of four Group companies that own Gestamp’s real estate assets in Spain. The transaction enabled Gestamp to keep full control of the assets for the operation of its industrial activity in Spain and had a direct impact on the company’s net debt.

In addition, the company has succeeded in extending the average maturity of its liabilities at a competitive cost, supported by the successful issuance of €500 million in senior secured notes and the execution of an amendment to its Senior Facilities Agreement (SFA) for a total amount of €1.7 billion (€1.2 billion in senior financing and €500 million in revolving credit), which resulted in extended maturities and improved terms and conditions.

Efficiency improves and free cash flow increases

In 2025, Gestamp continued to promote an efficient investment strategy to strengthen its competitiveness while ensuring the delivery of sustainable value to shareholders. This approach enabled the company to increase its Return on Capital Employed (ROCE) to 15.8%, compared with 15% in 2024.

In addition, the company’s free cash flow reached €278 million during the year (excluding the impact of the ‘Phoenix Plan’), above the €178 million recorded in 2024 and exceeding the target set for the year.

The figures achieved in terms of free cash flow and leverage have enabled Gestamp to meet its updated guidance for 2025 and to further strengthen its profitability drivers and balance sheet.

Outlook for 2026

Outlook for 2026

S&P Global Mobility does not forecast market growth for 2026 and anticipates divergent dynamics across the key regions where Gestamp operates.

In this context, in which uncertainties and cost pressures are likely to persist, alongside a moderate but less volatile penetration of electrified vehicles, Gestamp will continue to focus on reinforcing its financial positioning, strengthening its balance sheet, ensuring efficient investment, improving profitability, and implementing flexibility measures that will enable the company to surpass its current EBITDA margin by 2026 and achieve an operating cash flow conversion ratio of around 35%.

Gestamp has a solid order backlog of €47.5 billion for the next five years.